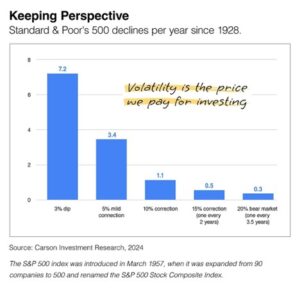

Market Volatility

Market volatility is part of the investing process. More than 7 times a year investors should expect pullbacks of 3 percent and, at least once a year (since 1928), investors should be prepared for a 10 percent correction. When viewed from a historical perspective, recent market activity isn’t as abnormal as one might think.

What a $5 Frappuccino Can Teach Your Teen

If you’re looking for one conversation that could change how the teens and young adults in your life think about money, start with their coffee order.

The $5 Frappuccino could be worth half a million, a daily $5 frappuccino costs $1,825 a year. That’s not a lecture, it’s just math. Now show your teen what happens if they put even half of that into a Roth IRA starting at age 18. At a hypothetical 8 percent average annual return, $1,000 a year grows to nearly $500,000 by age 65. And because it’s a Roth, the growth is tax-free, potentially $233,568 more than the same money in a taxable account over that period.1

You don’t have to convince a teenager to give up coffee forever. You just have to make the invisible visible. Once they can see what small daily choices actually cost over time, something shifts. That’s the foundation of financial literacy, and it doesn’t require a textbook. It just requires real decisions with real consequences.

Here’s How to Build on That…

Skip the Lecture. Hand Them Cash Instead. One of the most powerful teaching moments is also one of the simplest. Instead of heading to the store with a credit card, give your teen a fixed amount of cash for back-to-school or college shopping and let them keep whatever they don’t spend. The dynamic changes instantly. Every purchase comes with a visible trade-off, and spending less offers a direct, personal reward. The Frappuccino math comes to life in real time: is this $40 shirt worth it, or would I rather pocket the difference? The key is to stand firm and not pull out the plastic to cover a shortfall.

- A Budget Is Not an Allowance, It’s a Decision-Making Tool. Try assigning a clothing budget that covers everything: shoes, athletic gear, formal wear, and even basics like underwear. Help them map out anticipated needs at the start, then step back. If they blow through the budget early and can’t afford what they need later, that discomfort becomes the lesson. It’s the same principle as the Frappuccino. Every dollar only gets spent once, and choosing where it goes is the skill that matters most.

- Let Them Make Mistakes On Purpose. This is the hardest part for most parents. But a poor decision that leads to real inconvenience teaches more than any hypothetical warning ever will. The teen who runs out of clothing budget in October remembers that lesson in a way that no spreadsheet could replicate. As long as the consequences are manageable, resist the urge to step in. Mistakes build the emotional memory that shapes better judgment later.

- Have “the Talk” Before They Buy the College Hoodie. One of the best pieces of advice we’ve heard from a high school counselor: have the money conversation before your child falls in love with a school. Set expectations about costs, trade-offs, and what you can realistically afford before the emotional attachment forms. A teen who understands that choosing one school over another could mean $100,000 in debt versus starting debt-free is making the same calculation as the Frappuccino, just with much bigger numbers.

- Before They Leave for College, Make Sure They Understand. How money actually flows: paychecks, taxes, and how quickly it disappears. That credit card minimum payments are expensive traps that can linger for years. How to protect themselves from scams, identity theft, and overdraft fees. And that even small amounts invested early matter more than large amounts invested later, which is exactly where this conversation started.

The Real Payoff Goes Beyond Money: Teens who develop financial confidence tend to carry it into career decisions, relationships, and life choices. While 30 states now require a personal finance course before high school graduation, there is no substitute for what kids learn through real experience at home.2

The most effective financial education is quiet and cumulative. It starts with something as small as a $5 coffee and builds into a way of thinking that lasts a lifetime. It’s not about perfection. It’s about giving young people the space to make decisions, learn from the results, and build judgment over time.

If you’d like to talk through strategies for any of this, from setting up a Roth IRA for your teen to structuring a first budget, we’re here to help.

- Calculator.net, January 2026. Remember, to qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a 5-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

- Next Gen Personal Finance, October 9, 2025

Healthcare Costs in Retirement

In a 2025 survey, only 41% of all workers had calculated how much money they would need to pay for medical expenses in retirement. Being aware of potential healthcare costs during retirement may allow you to understand what you can pay for and what you can’t.1

A retired household faces three types of healthcare expenses.

- The premiums for Medicare Part B (which covers physician and outpatient services) and Part D (which covers drug-related expenses). Typically, Part B and Part D are taken out of a person’s Social Security check before it is mailed, so the premium cost is often overlooked by retirement-minded individuals.

- Copayments related to Medicare-covered services that are not paid by Medicare Supplement Insurance plans (also known as “Medigap”) or other health insurance.

- Costs associated with dental care, eyeglasses, and hearing aids – which are typically not covered by Medicare or other insurance programs.

It All Adds Up: According to one study, the average total cost to cover healthcare expenses in retirement for a 65-year-old is $165,000.2

Should you expect to pay this amount? Possibly. Seeing the results of one study may help you make some critical decisions when creating a strategy for retirement. Without a solid approach, healthcare expenses may add up quickly and alter your retirement spending.

Source:

- EBRI.org, 2025

- Investopedia.com, June 11, 2025